The broad market had a small gap down that took the whole first 30 minutes to fill, and that was the high of the day. I mentioned in the Lab that based on the first 30 minute activity, I thought that the Institutional Range plays were going to be the key for the ES, and it was (see that section below). NASDAQ volume closed at 1.6 billion shares.

Net ticks: -7 ticks.

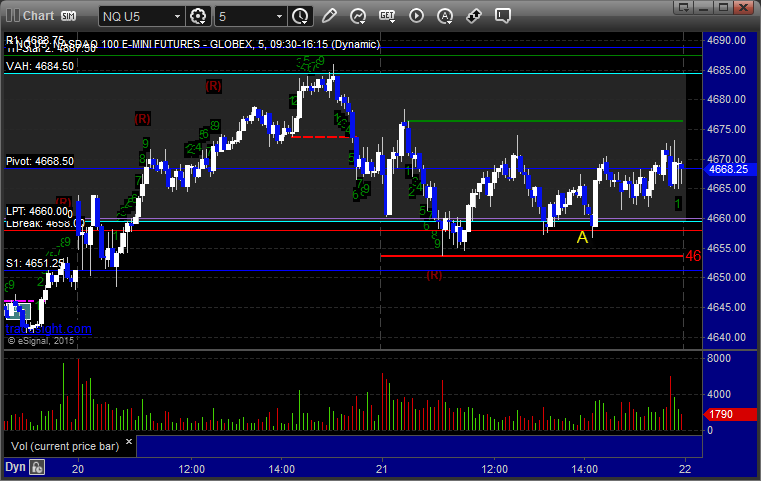

As usual, let’s start by taking a look at the ES and NQ with our market directional lines, VWAP, and Comber on the 5-minute chart from today’s session:

ES and NQ Opening and Institutional Range Plays:

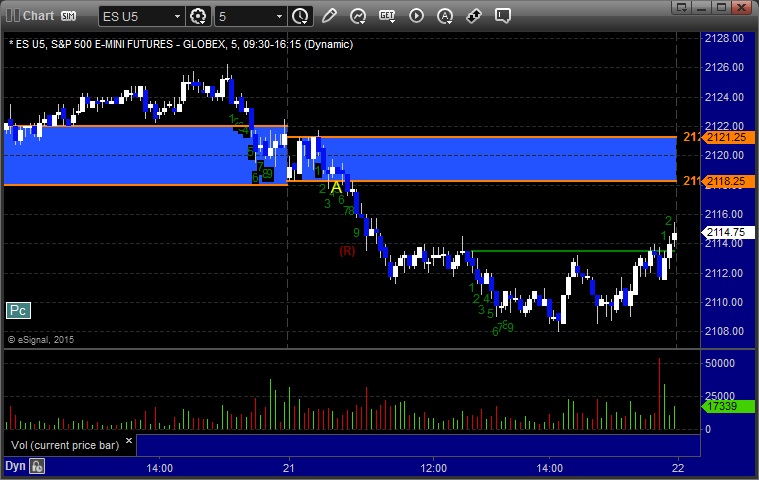

ES Opening Range Play triggered long at A and didn’t work, took foever, triggered short at B and eventually worked:

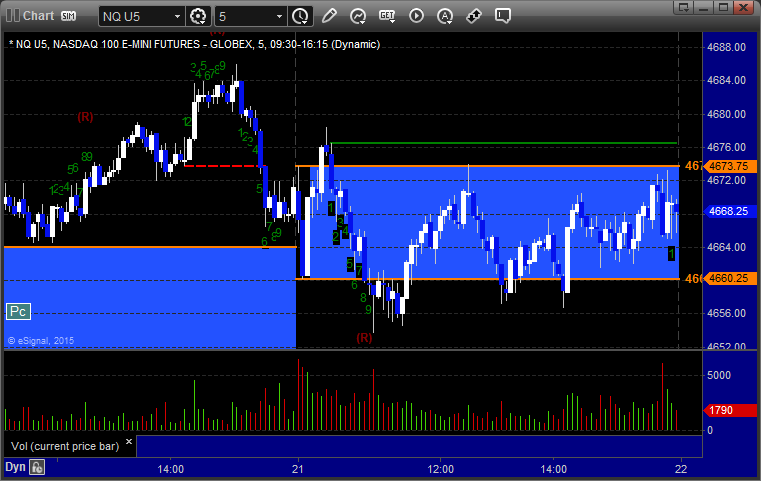

NQ Opening Range Play triggered short at A and worked enough for a partial:

ES Tradesight Institutional Range Play, as I mentioned specifically in the Lab as the key trigger, triggered short at A and worked great:

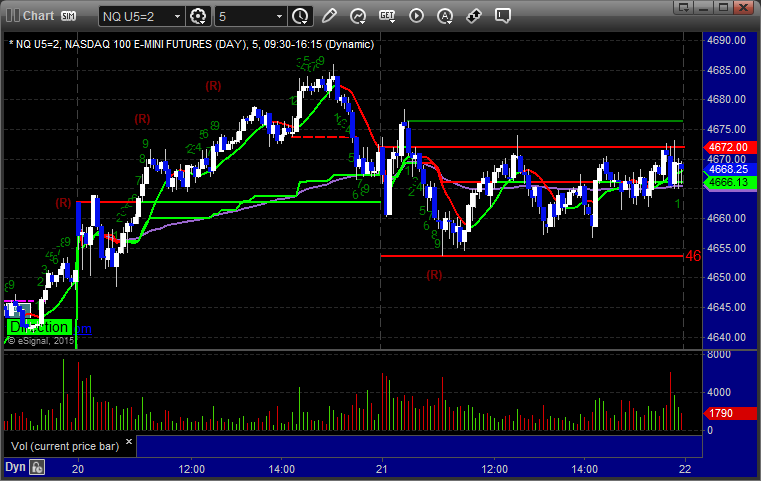

NQ Tradesight Institutional Range Play:

NQ:

Just a reminder that we use half points for ticks on the NQ and not the quarter point measurement that the exchanges switched to in recent years. This allows us to use 6 ticks as a key target as we do on the other contracts. It also keeps the value of a tick at $10, closer to the value of a tick on the other contracts.

Triggered short at A at 4657.00 and stopped for 7 ticks: